My Dear Extended Family:

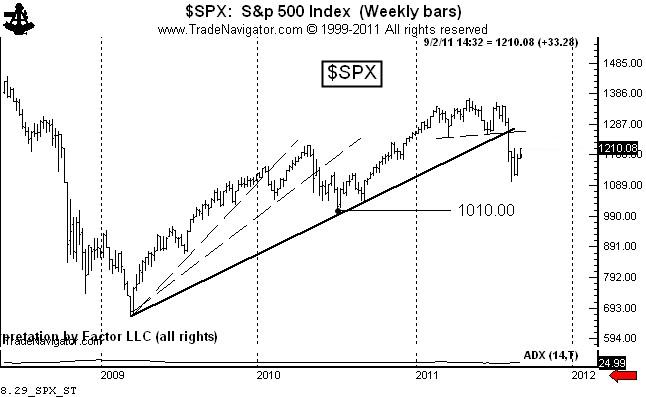

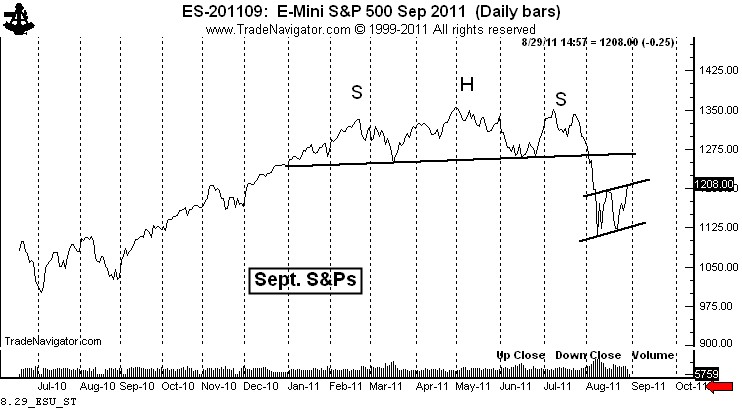

What is at the heart of the violent markets? The answer is Skier Illustration number 3.

Will Bernanke do something in the coming week? It does not matter in reality as business conditions are headed to a double dip in which the double could be wild on the downside. The Fed will act because of the balance sheet condition of the US and Western world financial industry devoid of false OTC derivative values.

Liquidity will be provided and Skier Illustration number 3 will take place, taking the US dollar lower and Gold to higher highs either now or very soon. As far as margin rates are concerned, they will rise to cash on both gold and silver before either sees full valuation.

You have heard from me on this gold reaction. Now hear from the extremely accurate Alf fields:

"The good news is that once the anticipated correction has been completed, gold should commence intermediate Wave 3 of Major 3. This should be the longest and strongest up-wave of the entire Bull Market. Expect high volatility and very high prices during that up-wave."

Now let's here from Kenny Adams, Master Technician, on long term trends:

"So far we have the potential for a topping action that may generate a moderate to deep correction - but not a long extended correction - not a termination of a bull trend."

Now lets hear from Dean of Gold, Harry Schultz:

"Don't bother me now. Call me when gold trades at $2400."

So stop worrying. At the worst this is a fast, deep correction before much, much higher prices for Gold.

Respectfully,

Jim

Jim