Thursday, May 31, 2012

Very Cool

This guy was shooting something with Bill Murray, and he and his friends wanted an autograph. Instead they got this - a slomo walk down a hallway, Wes Anderson style. The best part? Bill insisted on doing the slomo on set, not in post.

PIIGS Bigger Than You Think

"PIIGS" we are informed in the current Wikipedia entry "is a pejorative acronym used to refer to the economies of Portugal, Italy, Greece and Spain. Since 2008, the term has included Ireland, either in place of Italy or with an additional I."

With apologies, I am joining the ranks of contributors to such august publications as the New York Times, Wall Street Journal, Financial Times and The Economist who have used this handy label as a linguistic convenience and, I believe, with no aspersions intended.

My topic is the relative size of these five countries in a basic economic sense -- to one another and to the world as a whole. To make comparisons, I'm using GDP based on purchasing power parity (PPP). My source for the data is the IMF (International Monetary Fund), specifically the IMF's World Economic Outlook Databases.

The complete IMF database includes over 180 countries. For the chart below, I used the 58 countries with the largest GDP, which thereby includes the newcomer and smallest of the PIIGS (both in size and GDP) -- Ireland.

As an aside, anyone who is curious about the relative size of these five nations in a more conventional non-economic sense, the adjacent table arranges them in order of population along with the square miles and the GDP percent of world total. My source for geographic size and population is the Central Intelligence Agency's World Factbook.

The financial threat of Greece to the Eurozone and a potential spillover to the rest of the world has, of course, been much in the news. My illustration of the relatively tiny contribution of Greece to world GDP, should not be construed as an effort to downplay the reality of the financial risk it poses. The complex financial and political interlinkage of debtors and creditors trumps an easy metric such as GDP.

The PIIGS are Big!

The bar chart above does suggest the rationale for the broader anxieties about potential risks posed by the financial stresses in Spain and Italy. To put the size issue in a broader context, consider this: The European Union, which I didn't include in the chart above, would be the largest entity if I had. It's about 4.8% larger than the US based on GDP purchasing power parity. The PIIGS collectively constitute about 5.05% of world GDP, but they account for 25% of the GDP of European Union.

The world is worried about the PIIGS, and it should be.

Read more: http://advisorperspectives.com/dshort/commentaries/Sizing-the-PIIGS.php#ixzz1wRpCNcWN

Wednesday, May 30, 2012

Tuesday, May 29, 2012

Not Looking So Good

With the latest Case Shiller data out, look for the usual confusion between annual seasonal improvements and the regular

Case-Shiller:

“Home Price Indices data through March 2012 showed that all three headline composites ended the first quarter of 2012 at new post-crisis lows. The national composite fell by 2.0% in the first quarter of 2012 and was down 1.9% versus the first quarter of 2011. The 10- and 20-City Composites posted respective annual returns of -2.8% and -2.6% in March 2012. Month-over-month, their changes were minimal; averagehome prices in the 10-City Composite fell by 0.1% compared to February and the 20-City remained basically unchanged in March over February. However, with these latest data, all three composites still posted their lowest levels since the housing crisis began in mid-2006.”

Note that the table of Metropolitan regions is still showing composite year iover year price decreases:

Source: S&P Indices and Fiserv

Data through March 2012

Data through March 2012

Monday, May 28, 2012

Sunday, May 27, 2012

Saturday, May 26, 2012

Friday, May 25, 2012

Thursday, May 24, 2012

IWM

The IWM ETF represents the Russell 2000 small cap growth index. This ETF peaked at 84.66 this spring and has fallen in the the 74′s before the recent two day bounce. What we are looking at is a possible 5 wave rally from October into March, and now a possible 3 wave correction (Wave 2) of 38-50% of that entire 5 wave rally. Elliott Wave theory is broken down into 5 wave and 3 wave movements in the markets and individual stocks, where a full 5 wave pattern in a Bull market is obviously bullish and a 3 wave pattern corrective of the prior 5 wave rally.

The small cap index peaked with the reset of the market in March of this year, interestingly about 3 years into the Bull Market. The first low so far was a typical 38% fibonacci retracement of the rally from October through early March. The next low pivot would be a 50% pullback. This would place the IWM target around 72.10 plus minus some pennies.

In the 72′s that would represent a C wave decline that is equivalent to 161% of the A wave decline in the chart below from the 84.66 highs. ABC declines are common in a Bull cycle and are designed to throw investors off the back of the Bull. Normally the C wave is where investors finally throw in the towel near the bottom, as we saw in early October of 2011. I wrote an article on October 3rd last year, one day before the bottom outlining why a massive rally was about to ensue. Will we see the same thing now?

Well, this correction could indicate one more possible decline of 4-5% worst case should this projection in the chart below fulfill.

That said, the 38% retracement we have had so far would also qualify as a Wave 2 low last Friday. Therefore, this outline is to give you some indications of what to watch in case we drop further and pierce those lows. If we can hold this rally and rebound smartly again, then the C wave of the ABC is likely over and we can get an all clear to be more aggressive. . . .

Wednesday, May 23, 2012

Double Wow!

The national unemployment rate gets lots of attention, and lately more attention has been paid to the workforce participation rate since more Americans have given up looking for a job, but we can also see that an astounding 100 million Americans don’t have jobs.

Specifically, these are people who are part of the civilian over-16 non-institutional population who are either unemployed or not part of the workforce. According to the April jobs report, the number of jobless American stood at 100.9 million.

That’s an all-time record and it’s an increase of 26.2 million over the last 12 years. It’s as if we absorbed the entire adult population of Canada and not a single person had a job.

The numbers are staggering. The jobs-to-population ratio peaked 12 years ago. If we were to have the same ratio today, we would need 15.3 million more jobs, or 23.7 million fewer people.

(Note: The chart above is the Civilian Over-16 Non-Institutional Population minus the seasonally adjusted Civilian Workforce.)

Tuesday, May 22, 2012

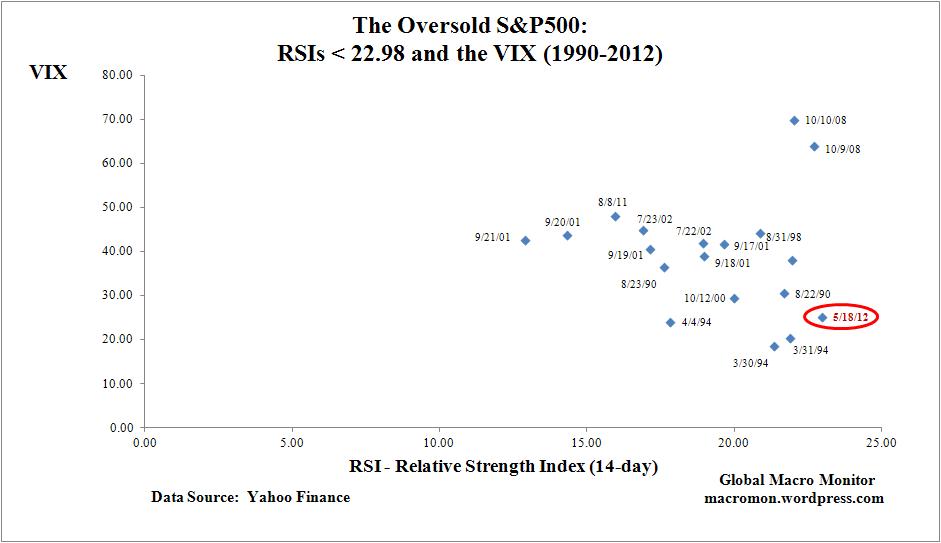

Undervalued? You Think?

Gold mining stocks, as measured by the AMEX Gold Bugs Index (HUI), are down nearly 40% from their August 2011 high. Representative ETFs such as GDX and GDXJ as down similar amounts, if not more. Mining company stock prices look to be falling into the abyss.

While buying mining stocks here could certainly look foolish in the near-term, NOT accumulating positions, or selling them for that matter, is likely to be the bigger mistake over the long term.

Gold mining stocks are attractive here for three primary reasons:

1. The sentiment on gold, and gold mining stock in particular, is at extreme bearish levels.

2. They are historically very cheap by a variety of relative and absolute measures of valuation.

3. The macro environment is likely to turn very supportive, thereby improving the fundamentals of the stocks, reversing the negative sentiment, and driving the valuations higher. . . .

Monday, May 21, 2012

Sunday, May 20, 2012

Saturday, May 19, 2012

Bear Is In Charge

The $OEXA200R (the percentage of S&P 100 stocks above their 200 DMA) is a technical indicator available on StockCharts.com that can be used to forecast conservative entry and exit points for the stock market.

The OEXA is used to find the "sweet spot" time period in the market when you have the best chance of making money. See Is This the Best Stock Market Indicator Ever? for a discussion of this technical tool.

The charts below are current through Friday's close.

Daily OEXA200R past 12 months

Monthly OEXA200R since April 2007

Interpretation:

The OEXA200R closed out the week at 55%.

Of the three secondary indicators:

- MACD has crossed and is NEGATIVE (red line above black).

- Slow STO has flipped from positive to NEGATIVE.

- RSI is below 50 and is NEGATIVE.

Commentary

Well, hang on. Here we go.

On May 15, the OEXA200R closed out the day at the critical 65% level, the point at which it is advisable to sell all long positions in anticipation of a major market decline. Since mid-2007, the starting point of the Great Recession, the OEXA200R has dropped to the 65% line on 25 July 2007, 16 October 2007, 6 May 2010 and 15 June 2011. In hindsight, each of these dates turned out to be auspiciously timed exit points preceding major downturns. See the "Background" section below for a fuller explanation of the significance of this metric.

The final phase of the mathematically inevitable Euro zone asphyxiation and disintegration is under way. Operation Twist is scheduled to conclude at the end of June. An Israeli – Iran conflict and oil spike are likely to follow before autumn. Taken together, the three are going to produce some very nasty and unpredictable synergy. The "Perfect Storm of 2012" has begun.

What is particularly disturbing is the velocity with which OEXA200R has crashed - from 89% to 55% since May 1. At this point, all bets are off. There may be a small rebound in the next month but even so, that would just be a "bear trap" for incautious traders. More likely, the Euro implosion will quash even that brief flicker of hope. Think about this: In the coming mid-June Greek elections, the betting now is that the far Leftists and Communists will come in first and likely even gain a majority. How's that going to affect investor confidence? It's just one indication of how insane the European situation has gone. For all of the above reasons, the most prudent course right now is to just sit on your cash, watch and wait. . . .

Weeks Away From Bottom

The current correction is creating very oversold conditions on intermediate-term indicators, like the ITBM (breadth) and ITVM (volume). While oversold indicators often signal final price lows for a correction, extremely oversold readings are a sign that the price low for the correction probably won't arrive until weeks after the extreme indicator lows.

On the chart below I have annotated two very good examples of this process. The red arrows show where indicator lows occurred, and the green arrows show the correction price lows, which arrived several weeks later after prices bounced out of the first low.

While a simialr circumstance seems to be setting up at present, in order to replicate the two previous examples I think the ITBM and ITVM need to go down a little more, and the PMO (Price Momentum Oscillator) needs to go down a lot more.

Conclusion: Current oversold indicator readings may offer hope that we will soon see a low for this correction; however, oversold conditions are approaching such extreme levels that we should anticipate that the correction will continue for several weeks before a significant low is reached.

We should also note that the two examples cited occurred during a bull market advance. If a bear market has begun, the resolution could be much more severe.

http://blogs.decisionpoint.com/chart_spotlight/2012/05/20120518-cs.html

Friday, May 18, 2012

VIX About to Jump!

A bullish reverse “Head & Shoulders” pattern appears to be developing on the CBOE S&P 500 Volatility Index (VIX) suggesting that a sharp move higher in this index is likely to occur soon. While bullish for buyers of “volatility”, this pattern is clearly bearish for the S&P 500 Index, since there is a high inverse correlation between the two.

Thursday night’s revelation of J.P. Morgan’s unexpected “hedging” loss of roughly $2B, along with worries that similar losses could be present on the balance sheets of other big banks has clearly moved to the “front line” of investor fears. The impact of last week’s European elections and the policy shifts that they imply, have also altered the uncertainty factor that trouble investors.

A series of sub-par trading sessions (volume wise), a cloud of relative indifference to either good or bad news, and the sense that investor confidence is eroding again has resulted in a period of “range trading” in recent weeks, despite higher-than-expected consumer confidence readings.

A decline in commodity prices along with persistently low 10-year Treasury and Bund yields might be viewed as evidence that capital is shifting away from risk assets and into assets that are perceived to be “safe”. While the “safety” issue is debatable, the expectation for another round of quantitative easing is growing. Before such an announcement could be made by the Federal Reserve, however, a broad based selloff in equity prices might occur first.

Thursday, May 17, 2012

Fractional Reserve Banking Exposed

Updating those parameters updates everything else automatically.

To view a time series of the iterations of the fractional reserve banking, simply click the “Show me in a table” button. Frackin’ Reserve will create an HTML page with a table for you, and open it in your default browser. This is a table made using the default parameters:

| Iteration # | Deposited by Customer | Amount Held in Reserve from Deposit | Amount Currrently Available to Lend Out from Deposit | Total Amount that “Can” be Lent Out | Total Amount that Has Been Lent Out | Total Amount Held in Reserve | Total Amount that Customers Believe They Have | Amount of Interest for 10 year(s) @ 5.0% on Loaned Money CAN NEVER BE REPAID! |

|---|---|---|---|---|---|---|---|---|

| 1 | 1,000.00 | 100.00 | 900.00 | 900.00 | 0.00 | 100.00 | 1,000.00 | 0.00 |

| 2 | 900.00 | 90.00 | 810.00 | 1,710.00 | 900.00 | 190.00 | 1,900.00 | 582.31 |

| 3 | 810.00 | 81.00 | 729.00 | 2,439.00 | 1,710.00 | 271.00 | 2,710.00 | 1,106.39 |

| 4 | 729.00 | 72.90 | 656.10 | 3,095.10 | 2,439.00 | 343.90 | 3,439.00 | 1,578.06 |

| 5 | 656.10 | 65.61 | 590.49 | 3,685.59 | 3,095.10 | 409.51 | 4,095.10 | 2,002.56 |

| 6 | 590.49 | 59.05 | 531.44 | 4,217.03 | 3,685.59 | 468.56 | 4,685.59 | 2,384.61 |

| 7 | 531.44 | 53.14 | 478.30 | 4,695.33 | 4,217.03 | 521.70 | 5,217.03 | 2,728.46 |

| 8 | 478.30 | 47.83 | 430.47 | 5,125.80 | 4,695.33 | 569.53 | 5,695.33 | 3,037.92 |

| 9 | 430.47 | 43.05 | 387.42 | 5,513.22 | 5,125.80 | 612.58 | 6,125.80 | 3,316.44 |

| 10 | 387.42 | 38.74 | 348.68 | 5,861.89 | 5,513.22 | 651.32 | 6,513.22 | 3,567.10 |

| Fractional Reserve Banking is EVIL. | ||||||||

You can set your own parameters and create any table you want. This is useful to see exactly what is happening at each iteration in the process, and how it grows like an out-of-control brush fire.

Using Frackin’ Reserve!

Frackin’ Reserve! is super simple to use. Simply change the parameters, and everything is updated automatically. Here’s a quick rundown of what each parameter and output result is:

Initial Parameters for Fractional Reserve Calculations

Initial deposit: This is the first “kick-starter” for the whole system. It puts some money into the banking system, and is the foundation for all subsequently created fiat money.

Fractional reserve factor: This is expressed as a factor, though most often it is expressed as a percentage. It is also called the “reserve requirement”, “cash reserve ratio”, or “reserve ratio”.

Iterations: This is the number of times that people deposit money into the system. The first iteration is the initial deposit. All subsequent iterations are loans, create fiat (fake) money, and bear interest.

Fractional Reserve Results on the Money Supply

What customers think they have: This is the running sum of what all customers have deposited into the banking system.

What the bank has in reserve: This is amount of the initial deposit that the bank actually has kept back in reserve. It is a running sum.

What the bank can loan out: This is the amount that the bank has the right to loan out from all past deposits. It is a running sum.

What the bank has loaned out (fake money): This is the actual amount loaned out by the bank. On the first iteration, it is zero. It is a running sum.

What the bank’s next loan is: This is the amount that the bank’s next loan will be. It is always smaller than the previous one. It is not a running sum.

Interest Owed Parameters

Interest periods (in years): This is the number of years that you wish to calculate compound interest on.

Interest rate ( × 100 = %): This is the interest rate expressed as a decimal. Multiply it by 100 to get the percentage.

Compounded: This is how you wish the interest to be compounded. It can be one of annually, monthly, daily, hourly, by the minute, by the second, or by the “tick”. A tick is a unit of measurement, and there are 10,000,000 ticks per second.

Interest Owed Results

Total interest on money lent out: This is the amount of interest owed on all loans. It does not include the principal; it is only the interest.

Total interest and principal: This is the total of all the interest and the principal. It is equal to the “Total interest on money lent out” plus the principal.

It should be noted that Frackin’ Reserve! is a simple simulator, and does not take into account the rate of iterations. This is largely an academic point though, and doesn’t really matter all that much. It is only useful if you want to know what the state of things are at some particular point in time for a given rate of loans. i.e. it has no bearing on illustrating the way fractional reserve banking works. The iterations in reality are fast enough to discount the rate as being unimportant. The short and simple version of that is that Frackin’ Reserve! assumes that all loans and deposits for all iterations are made at the same time. If you don’t understand what that means, then don’t worry. It’s really only a minor technical note for those that already know about how the system works. These are not the droids you are looking for…

Code Notes for Programmers and Non-Programmers

The source code is EXTENSIVELY commented with the express purpose of making it easy to follow for non-programmers.

So, even if you do not program, there’s lots of information in there, and it’s basically a tutorial on its own.

For programmers… It’s ugly. Yeah… I did naughty things because it’s easier to read for non-programmers that way. This is meant to be educational about fractional reserve banking, and not a programming tutorial. So, when you see everything stuck in 1 method, just remember that it’s all for a good cause.

Ryan Smyth is a Canadian expat currently living in Australia. He works in software, but is passionate about many current issues and the impending demise of freedom and privacy. He can be found blathering on (and sometimes ranting) at his blog, Cynic.me.

http://www.activistpost.com/2012/05/frackin-reserve-fractional-reserve.html#more

This Is What I Have Been Waiting For - DIVERGENCE

Smart money knows where the safe haven is and it is not the S&P 500...It is Gold baby!!!! 2000 oz by end of summer!!!

Wednesday, May 16, 2012

Should Have Headed The Warning About May

This chart shows what’s been happening with the market recently. The “sell in May” memo apparently didn’t get to everyone.

The three defensive ETFs; Staples ($XLP), Utilities ($XLU) and Healthcare ($XLV) aren’t doing so bad.

But the real damage is happening to the cyclical ETFs; Industrials ($XLI), Energy ($XLE) andMaterials ($XLB).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Subscribe to:

Comments (Atom)